Making Sense of Metrics Used by Lenders on Investment Commercial Properties

by: Todd A. Kuhlmann, CCIM

Loan-To-Value (LTV), Debt Service Coverage Ratio (DSCR), and Debt Yield are three important metrics used by lenders to determine the maximum loan an investment commercial real estate property. In this blog post, we'll discuss each metric in detail and explain why they are important to understand when investing and lending in commercial real estate.

Loan-To-Value (LTV)

Like residential loans, Loan-To-Value (LTV) is a ratio that compares the amount of a loan to the value or purchase price of the property being used as collateral. This ratio is expressed as a percentage and is used to determine the amount of risk a lender is taking on when providing financing. A lower LTV ratio indicates that the lender is lending a smaller percentage of the property's value, which is generally considered to be a lower risk.

For example, if a property is worth $1,000,000 and a lender provides a loan of $800,000, the LTV would be 80%. If the lender provided a loan of $700,000, the LTV would be 70%.

Lenders often have different LTV requirements based on the type of property and the loan amount. For example, a lender may require a lower LTV for a more speculative property, such as a new development, compared to a more established property with a stable income stream.

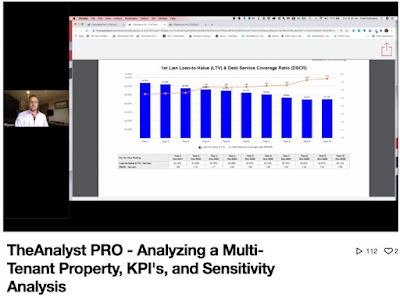

Debt Service Coverage Ratio (DSCR)

The Debt Service Coverage Ratio (DSCR) is a metric used to determine a property's ability to generate enough income to cover its debt obligations. This ratio is calculated by dividing the property's net operating income (NOI) by its total debt service. The NOI is the property's income after expenses and the debt service includes principal and interest payments.

For example, if a property has an NOI of $100,000 and Annual Debt Service (ADS) of $70,000, the DSCR would be 1.43 ($100,000 / $70,000). A DSCR of 1.43 indicates that the property generates enough income to cover its debt obligations 1.43 times over. Lenders typically will have minimum DSCR requirements of 1.20x to 1.40x based on the stability and risk associated with the property.

|

| Screenshot courtesy of TheAnalyst® PRO Investment Analysis Report |

Debt Yield

The Debt Yield is similar to the DSCR but is expressed as a percentage rather than a ratio. This metric is calculated by dividing the property's NOI by the loan amount. The Debt Yield measures the return a property generates on its debt investment.

For example, if a property has an NOI of $100,000 and a loan amount of $1,000,000, the Debt Yield would be 10% ($100,000 / $1,000,000). A low debt yield means that a property is not generating enough income to cover the loan payments. A good debt yield should be at least 10%, but the higher the percentage, the less risk for the lender.

|

| Screenshot courtesy of TheAnalyst® PRO Investment Analysis Report |

Why are these metrics important?

These metrics are important for lenders as well as borrowers to help them determine the risk involved in financing for a property. A property with a high LTV, low DSCR, and low Debt Yield would generally be considered a high-risk investment, which may make it more difficult for the property to secure financing.

TheAnalyst PRO makes the complex financial analyzation of commercial real estate easy. Gain access to our extensive key performance indicators (KPI’s) and investment measures including the LTV, DSCR and Debt Yield providing instant loan validation.

For more details on advanced KPI’s and other investment measures, we have created a full video on demand training center in TheAnalyst PRO.

Sign up for a Demo today to learn more about how TheAnalyst PRO can take your Commercial Real Estate business to the next level!

|